Attractive Opportunities in the Ultrapure Water Market

Ultrapure water is a growing market, with a significant number of global and regional players. The major companies operating in the global ultrapure water market are GE Water and Process Technologies Inc. (U.S.), Veolia Environment S.A. (France), Ovivo Inc. (Canada), Pall Corporation (U.S.), Dow Water & Process Solutions (U.S.), Koch Membrane Systems (U.S.), and Hydranautics (U.S.), among others.

Browse 96 market tables and 58 figures spread through 166 pages and in-depth TOC on "Ultrapure Water Market by Equipment, Materials & Services (Filtration, Consumables/Aftermarket, and Others), by Application (Washing Fluid and Process Feed), by End Use Industry (Semiconductors, Coal Fired Power, Flat Panel Display, Pharmaceuticals, Gas Turbine Power, and Others) & by Region - Global Trends & Forecast to 2020".

Speak to Analyst @ https://tinyurl.com/y2wlcsjv

The semiconductors end-use industry is expected to dominate the ultrapure water market by 2020

Ultrapure water in the semiconductors industry is expected to contribute the maximum share in this market by 2020. Increased demand for the high purity water in wafer fabrication and semiconductors industry is driving the growth in this segment. Apart from this industry, coal fired power plants, flat panel, and pharmaceuticals are other major end-use industries of ultrapure water.

Washing fluid segment to account for the highest share in the ultrapure water market by 2020

Washing fluid is the largest application for ultrapure water. Many end-use industries such as semiconductors, flat panel, and pharmaceutical use ultrapure water as washing fluid. Various processes in these industries require washing and cleaning in order to remove impurities and particles from the small parts, this is achieved through the use of highly purified ultrapure water. Apart from washing fluid, ultrapure water is also used as the process feed in coal fired power plants and gas turbine power generation companies.

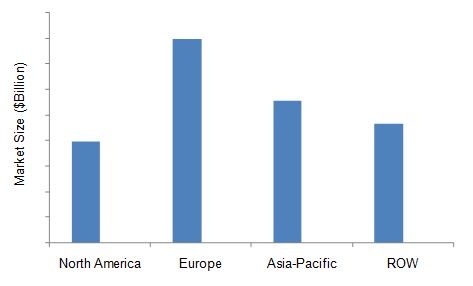

Asia-Pacific to dominate the ultrapure water market during the forecast period

Asia-Pacific accounted for the largest share of the ultrapure water market in 2014, followed by North America and Europe. The Asia-Pacific and North America regions are further expected to show a high growth in the future. The growth is attributed to the increased growth in the electronics industry which creates more demand for ultrapure water and installations of new coal fired power plants in Asia-Pacific.

Download PDF Brochure @ https://tinyurl.com/y234xh5z

These companies focusing on new product launches, agreements, contracts, mergers & acquisitions, expansions & partnerships have together accounted for 56% of total new developments in the ultrapure water market between 2011 and 2015.

For more Info Visit Blog: https://chemicalsresearchmarket.wordpress.com/blog/

The

The